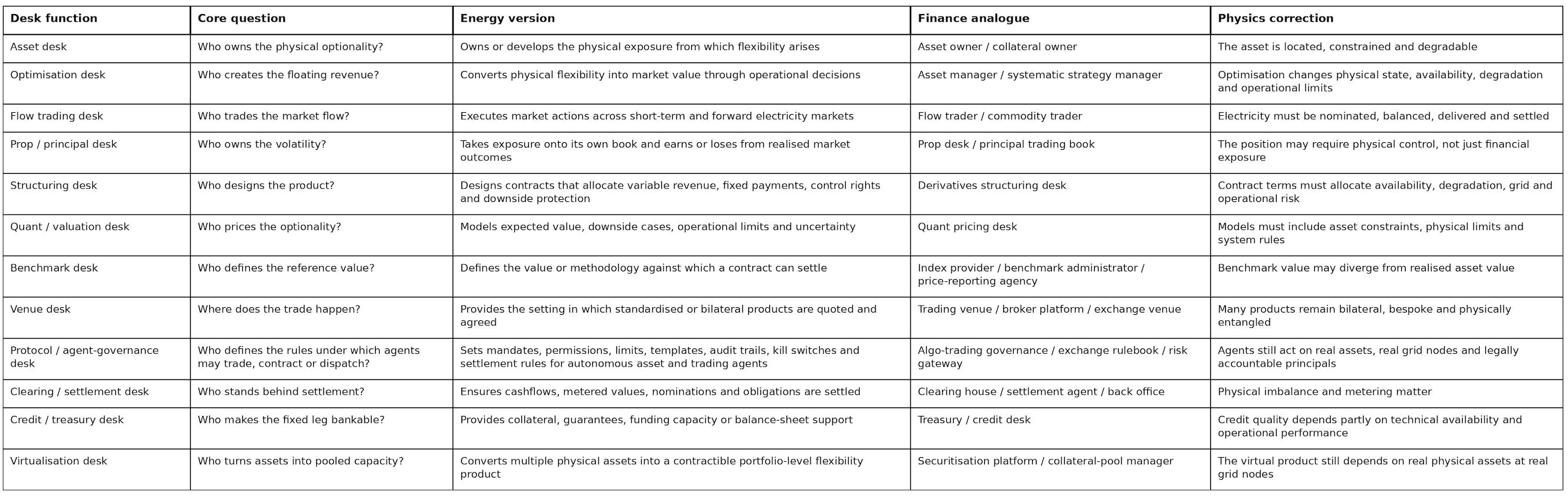

Energy Desks: a classification

The Market for Variability Swaps

Power-market volatility is creating new instruments and new roles. “Variability swaps” transform volatile power-market outcomes into fixed, floored, indexed or otherwise stabilised cashflows.

Energy Storage Systems and Variability Swaps

This is Part II on connections between symmetric energy assets and variance swaps. In Part I we recalled the basic principles of classical variance swaps and started adapting ideas to the energy markets.

Who are the trading desks in this emerging market, and what do they do?

Our starting point is a LinkedIn conversation in which Fortinbras and FlexPower were described as trading desks responding to volatility with new instruments: day-ahead swaps, BESS revenue floors, short-term PPAs.

FlexPower and Fortinbras are recognisably ‘desk-like’ in a financial sense: they structure risk, create products and may take positions.

But what about Entrix, ESFORIN, enspired, suena, or a virtualiser such as terralayr? They also perform trading-related functions. Are they ‘trading desks’?

Perhaps we need to expand our idea of what a trading desk can be: technology-led optimisers, aggregators, and virtualisers may soon be at the forefront of creating a new kind of trading desk. The power trading desks of the future might focus on developing ways for software-agents to originate, structure, execute, and manage variability swaps based on objective functions and remits set by their principals.

But before we become even more imaginative, let’s try to tie down the notion of a ‘trading desk’ in the energy context through analogy to finance.

In finance, a flow desk handles client trading. A prop desk trades the firm’s own book. A structuring desk designs products. A quant desk prices them. A risk desk constrains them. Index providers define a reference values. There are trading venues and clearing houses. Let’s think about energy industry analogues.

A desk is a function, not a company

A desk is a commercial function: a place where a certain kind of decision is made, price is formed, risk is owned, contracts structured, flow is executed, or exposure is transformed.

Energy firms often bundle several desk functions together. One company may optimise the asset, support structuring, provide the trading algorithm, advise on bankability, and perhaps even take some market risk. Conversely, one contract may split these functions across several parties: asset owner, optimiser, offtaker, lender, benchmark provider, and trading venue.

A desk answers a question.

Who trades the flow?

Who owns the volatility?

Who creates the floating revenue?

Who writes the product?

Who defines the reference value?

Who hosts the trade?

Who stands behind the risk?

Who controls the physical asset?

As the markets mature we may see clearer lines around these questions and corresponding specialisation.

Energy-desk taxonomy

The European flexibility market is not producing one new kind of firm. Instead, it is beginning to develop a ‘stack’ of functions.

It starts with the asset desk. This is the owner or developer of the physical exposure: batteries, renewable portfolios, CHP, industrial loads, distributed batteries, flexible demand, co-located assets.

Then comes the optimisation desk where physical flexibility connects to market dynamics: when to charge, discharge, reserve, rebid, hold back, or stay idle. Trading algorithms need to work against state of charge, degradation, warranty, grid connection, market access, imbalance exposure, and operational constraints.

The asset and optimisation desks set the framework for the atomic question: to cycle or not to cycle? Every decision sits at the intersection of physics, economics, and governance: is the asset within limits, is the spread worth capturing, and is the action permitted?

Next comes the flow trading desk. This is where short-term power is bought and sold. Day-ahead, intraday, balancing, ancillary, shape, spread, imbalance. The flow desk is where the asset’s optionality becomes market action.