BESS Zoom-In: Optimiser Transactions in Germany.

German Energy Transaction Notebook II. Provenance?

If it’s worth doing once, it’s worth doing twice, with zoomed-in attention the second time. Here’s a quick follow-on to our “Transaction Notebook” zooming in on flex-asset / BESS-focused optimisers.

Last time I said that flexible asset optimisation may be one of the most strategically attractive parts of the market.

It may also be one of the most exposed: exposed to consolidation, exposed to margin pressure, and exposed to the possibility that software moats here prove thinner than they first appear.

It’s an interesting question for every software driven company: how much of a ‘moat’ do you have with the new technology available? Have you set yourself up to take advantage?

I think for the actual mental load of being a person, interacting with these systems is going to be quite strange. I already find that I’m like: Am I keeping up with the ability of these systems to produce insights for me? How do I structure my life so I can take advantage of it?

Jack Clark, Transcript link

It’s hard enough as individual, even harder for a company. Gaps will develop quickly.

So, who has investor momentum? Who is burning through the cash? Who is growing organically? And who is investing in this ‘exposed’ part of the market? The transaction data can’t settle these questions, but it might help you form a view.

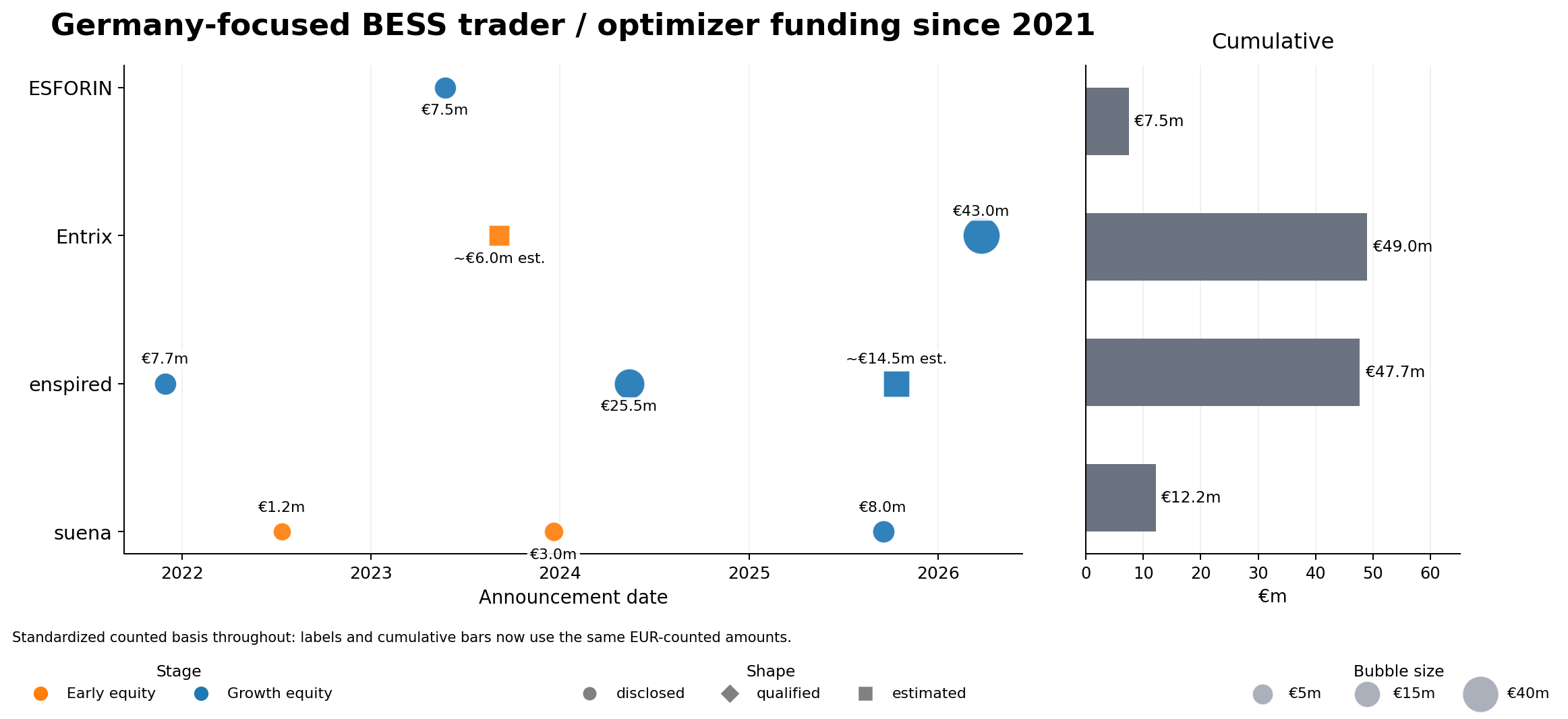

The first thing the funding history shows is that there is no single “optimiser market.” There are at least two capital stories. The trader / optimizer core (ESFORIN, Entrix, enspired, suena, with FlexPower better treated as an M&A signal than a funding case) still looks mostly like a venture-style story.

The adjacent layer (I’ve chosen to look at The Mobility House, Terra One, Flower, terralayr) already looks more like a commercialisation and financing story, where optimisation is increasingly tied to ownership, structured debt, or the control of asset portfolios.

The distinction matters because it explains why some transaction sizes look much larger than others: in several cases, investors are backing more than software and trading capability; they are backing businesses that sit closer to a wider base of assets and revenues. Over time we may see convergence.

The Core

Start with ESFORIN. Publicly, its funding history is short but revealing. In April 2021, SET Ventures announced growth capital for ESFORIN, but no amount was disclosed. What that early release did disclose was operating traction: ESFORIN said it had completed more than 2.2 million trades on EPEX in 2020 and expected more than €100 million turnover in 2021. Then, in May 2023, the picture became clearer with a disclosed €7.5 million Series B led by SEB Greentech VC, with participation from ERAME, SET Ventures, Christoph Ostermann / Green Fortress, and ESFORIN’s founder holding.

The sequence suggests a business that was commercially established before further venture expansion. It also helps explain why ESFORIN might be underestimated if one looks only at disclosed funding totals: the company may simply have needed less outside capital, or preferred to raise less, because it sits closer to flex-structuring and market access than to a pure “AI for batteries” pitch.

With Entrix we see three stages. First, there is an inception investment in summer 2021 from Pelion Green Future, though no public amount was disclosed. Entrix’s own 2023 announcement says Pelion had already invested “during its inception in the summer of 2021.” Then, in September 2023, Entrix announced a new financing round with Abacon Capital, Enpal, KRAFTWERK.ventures, Pelion Green Future, and several business angels, but the company did not publish a round size in its own release. The clearest number only appears indirectly in industry coverage: Energy-Storage.news reported that Entrix’s CEO said total funding had exceeded €8 million to date, with the vast majority coming from the latest round. In March 2026, a cleaner disclosure: €43 million round led by Junction Growth Investors and Korys, alongside BNP Paribas’ Solar Impulse Venture Fund, Allianz, AENU, Enpal, Abacon, and Arvantis.

The Entrix story does not look like a smooth “Series A, Series B, Series C” staircase. It built early backing quietly, added sector-heavy investors in 2023 without disclosing the amounts then reappears in 2026 with a large, clearly disclosed jump. What might one conclude from this sort of pattern? A business that needed time to prove commercial traction before the larger round? Or simply a company whose early rounds were raised in a less publicity-driven way.

Contrast enspired’s funding growth, which is much easier to read. In December 2021, it announced a USD 8.7 million Series A to expand grid-flexibility optimization in Europe. In May 2024, it announced a clearly disclosed €25.5 million Series B led by Zouk Capital, with a broad syndicate including PUSH VC, Banpu NEXT, Vopak Ventures, Presidio Ventures, Emerald, Helen Ventures, 360 Capital, and EnBW New Ventures. Then in October 2025, enspired said it had extended Series B to over €40 million, bringing in Future Energy Ventures while existing investors also recommitted. This is ‘textbook’ successful venture progression. That ‘staircase’ shape suggests that enspired has repeatedly been able to refresh investor conviction in a way that is both gradual and visible. No reset needed.

suena has been funded at a smaller scale. It’s important to note that suena has a different setup. Their execution is built on Volue PowerBot, with Suena’s focus on adding optimisation intelligence above that layer.

It is worth noting that external coverage often describes Suena as a “platform.” For example, PV Magazine reported in early 2024 that they had secured financing to scale their “AI-based trading platform” for renewables and storage. Yet Suena’s own branding is more restrained: “Autopilot” rather than “platform.” This gap highlights how loosely the term circulates in the energy sector, sometimes applied to any digital optimisation service. Their execution is built on Volue PowerBot, with Suena’s focus on adding optimisation intelligence above that layer.

The public history runs from a €1.2 million pre-seed in July 2022, to a €3 million seed round in December 2023, to an €8 million Series A in September 2025. The 2025 Series A was led by Eneco Ventures with 4impact participating, while earlier backers such as InnoEnergy, J.O.S.S., Santander, and Energie 360° also returned.

Adjacent Players

The adjacent group tells a more dramatic story because the financing forms are already different.