German Energy Transaction Notebook

2024-2026 YTD

A review of publicly announced energy-linked transactions with German exposure from 1 January 2024 to 29 March 2026. Estimates, comparisons, analysis based on publicly available data.

Between 1 January 2024 and 29 March 2026, a revealing set of publicly announced transactions accumulated around the German energy market.

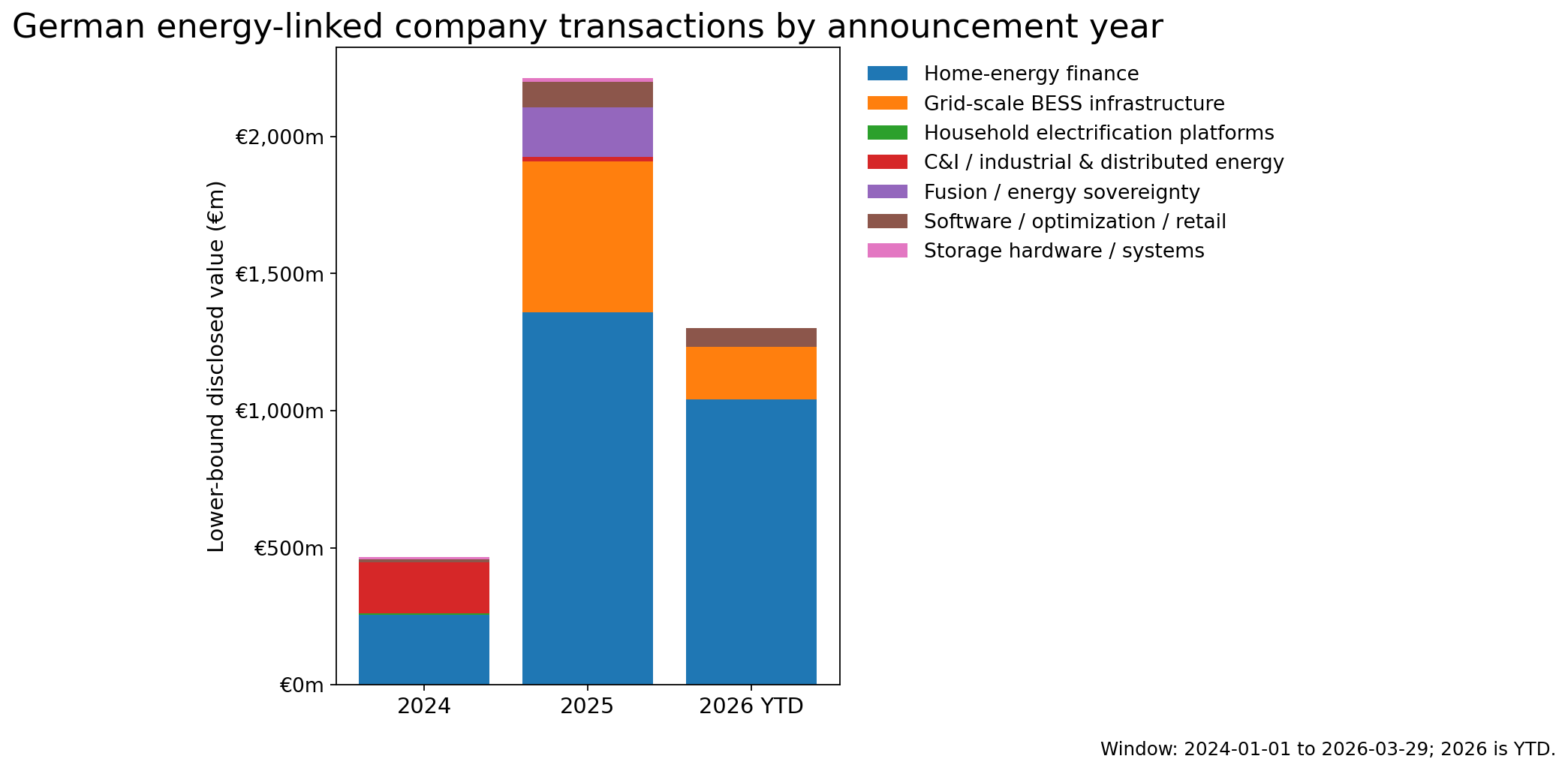

This review captures 27 company-announced transactions notionally worth €3.98 billion on a lower-bound basis, alongside 14 investor-led private-capital entries, of which 9 disclosed or bounded amounts totalling €21.48 billion. The company-side sample is small in 2024, 6 deals worth €466 million, before broadening sharply in 2025 to 16 deals worth €2.21 billion, with 2026 year-to-date already at €1.30 billion across 5 deals. That progression is part of the story: the larger capital-formation layer of the Energiewende becomes much more visible only later in the sample, especially as household-electrification finance, battery platforms, and grid-linked capital start to scale.

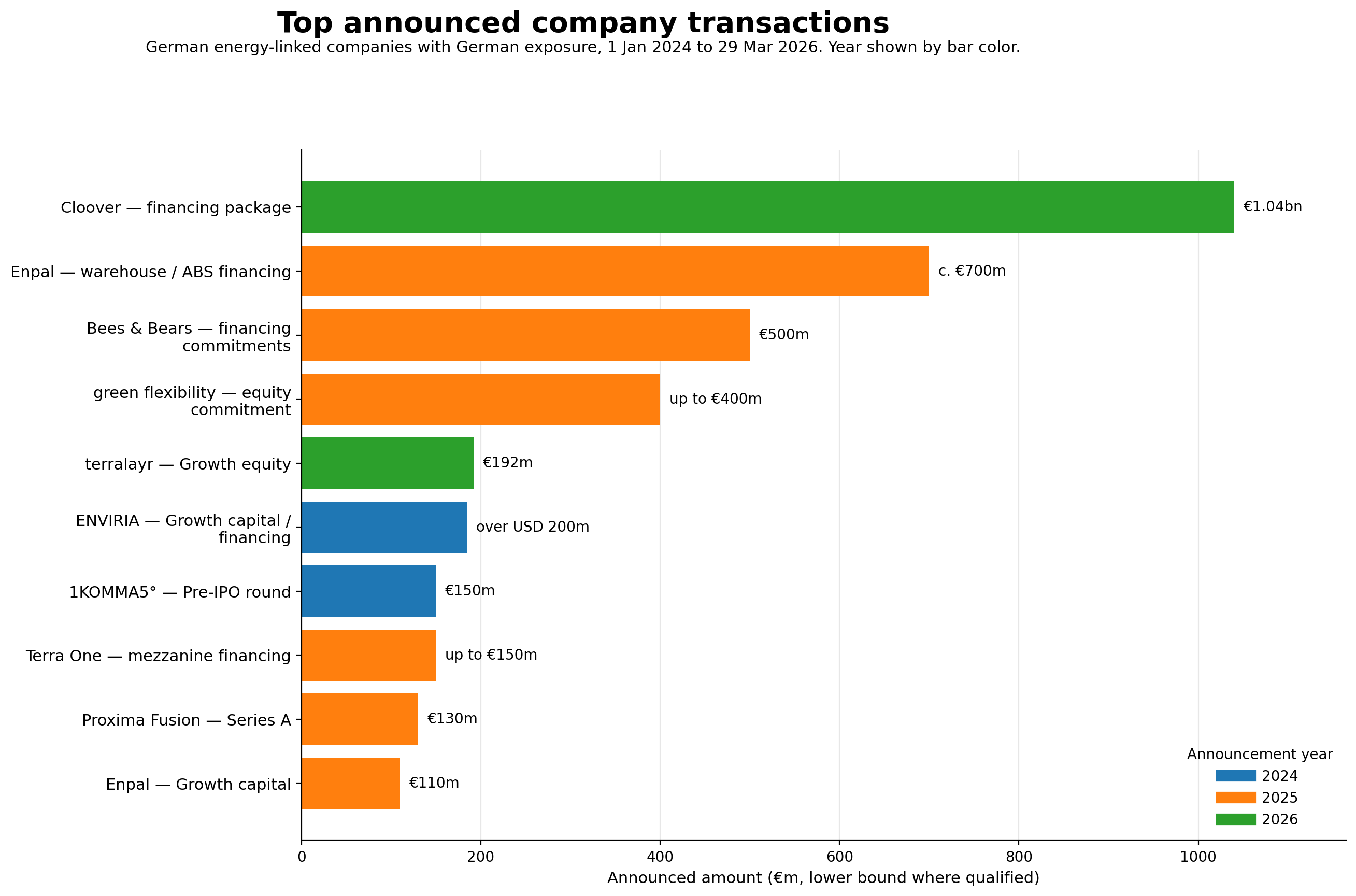

The top 10 distinct deals/transactions in the sample are…

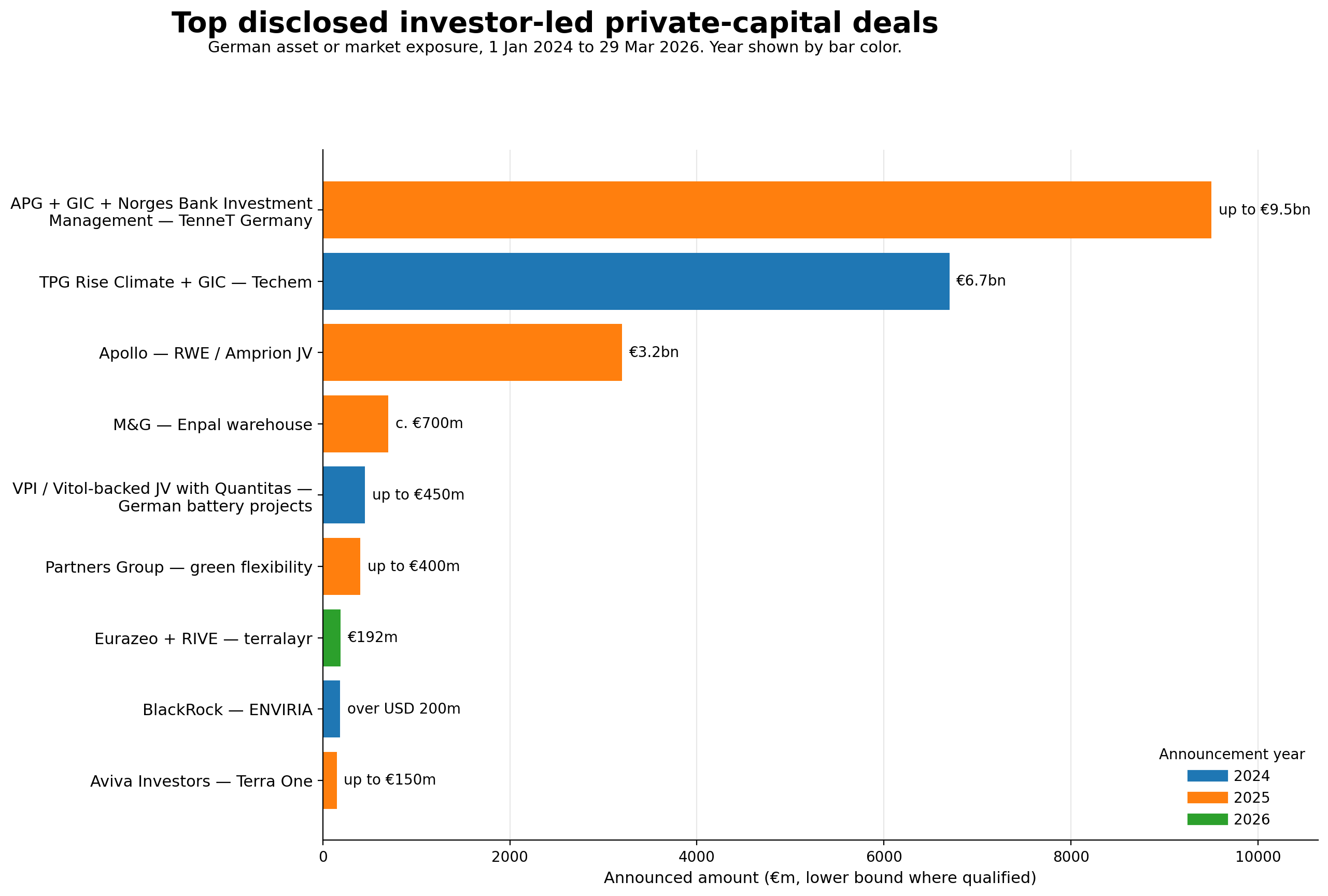

APG / GIC / Norges Bank IM — TenneT Germany: up to €9.5bn

TPG Rise Climate / GIC — Techem: €6.7bn

Apollo — RWE / Amprion JV: €3.2bn

Cloover — financing package: €1.04bn

Enpal / M&G — warehouse: c. €700m

Bees & Bears — financing commitments: €500m

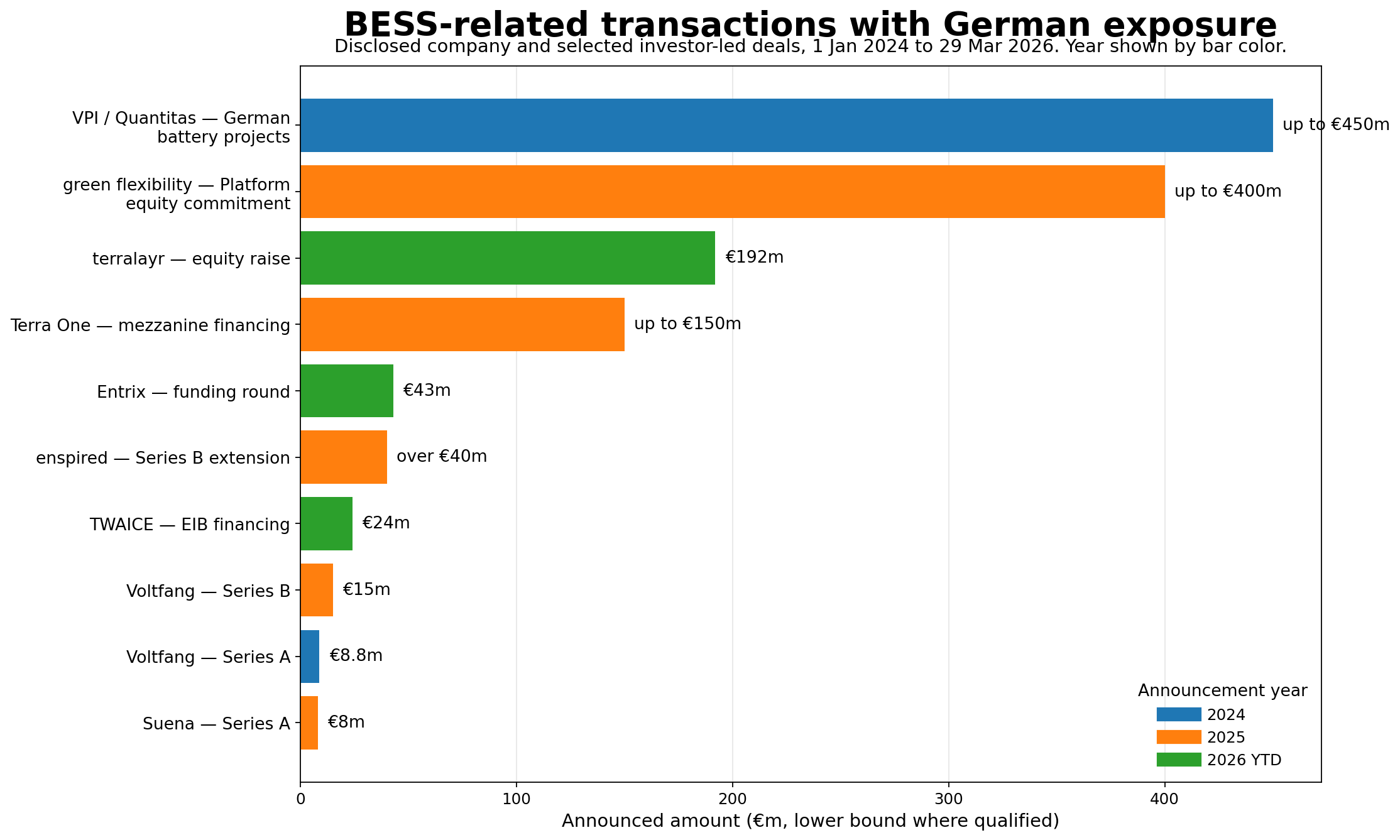

VPI / Quantitas — German battery projects: up to €450m

green flexibility / Partners Group: up to €400m

terralayr — equity raise: €192m

ENVIRIA / BlackRock: over $200m

The emerging dataset combines company rounds, mezzanine, warehouses and asset-backed structures, investor-led private-capital deals, and selected strategic transactions where Germany is the clear operational focus. There’s enough here to start reading patterns from the flows.

What kinds of capital are entering German energy, through which structures, and with what implied view of where value will sit next?

From the available data gathered so far, 2024 was an emerging build phase. By 2025, the pace and scale of transactions intensify. And 2026, even as a year-to-date slice, is already about half the announced transaction value in 2025.

We see different layers of the same market being developed and financed in parallel and in different ways.

BlackRock backed ENVIRIA with more than $200 million for commercial solar in early 2024.

EQT launched its Transition Infrastructure strategy in December 2024.

Partners Group committed up to €400 million of initial equity to green flexibility in January 2025.

Enpal and M&G announced a roughly €700 million warehouse in October 2025.

Apollo agreed a €3.2 billion structure tied to RWE’s 25.1% stake in Amprion

A consortium including APG, GIC, and Norges Bank Investment Management agreed to buy 46% of TenneT Germany for up to €9.5 billion.

Which companies in the German energy-linked space announced the biggest capital events? Let’s focus on the biggest company-level announced transactions in the dataset from the perspective of the company raising or receiving capital. For an overall view, we’ll mix things like: equity rounds, mezzanine, (ABS) warehouses, debt facilities, financing commitments.

At company level, the largest transactions do not cluster around one tidy category called “energy tech.” They gather instead around the capital-formation layer of the Energiewende: household electrification finance, battery platforms, and the structures that make distributed assets scalable.

What is being built here is not only technology deployment. It is the financing architecture that allows deployment to keep happening without every company funding every asset from scratch on its own balance sheet.

Enpal’s warehouse with M&G is one expression of that. Cloover’s package of equity, debt facility, and guarantee support is another. 1KOMMA5° sits in the same broader story even though the instrument differs. The household is becoming an energy asset base, and the prize is not just installation volume but the financed and controllable customer relationship.

This is also where competition sharpens. Enpal and 1KOMMA5° are not merely selling equipment. Both are trying to sit at the centre of the electrified home. thermondo approaches from a more focused heating angle. Cloover is different again: it does not primarily present itself as a consumer brand, but as enabling infrastructure for installers and financing flows. So this is not simply a fight over who sells more hardware. It is a fight over who becomes the dominant financing and operating layer around the home.

If that is one contest, then another one involves grid-scale batteries and flexibility infrastructure.

Germany’s battery and flexibility market now attracts an unusually wide range of capital. There is growth equity, mezzanine, infrastructure-style capital, project partnerships, and private-credit logic, all circling the same basic opportunity. green flexibility, Terra One, terralayr, ju:niz Energy, TotalEnergies/Kyon, Alpiq and others are all positioning around utility-scale storage. But they are not all the same kind of animal. Some are primarily developers and owners. Some are trying to become platforms. Some are building both an asset base and a commercialization layer.

The market strategically important and crowded. The competition is not only for megawatts and megawatt-hours. It is also for grid access, land, connection rights, route-to-market, capital efficiency, and the credibility to keep financing large asset bases as the field matures.

Consider terralayr, Entrix, enspired, Suena, and in Citadel’s acquisition of FlexPower: this is the control and optimization layer: dispatch, forecasting, revenue stacking, degradation management, and market access. In other words, a large part of the competition is about who gets the right to orchestrate flexible assets rather than merely own them. terralayr is interesting here because it is also building its own battery assets, thereby seeding its commercialization and flexibility platform.

Each sits differently along the Smiling Curve. Each faces the gravitational pull of the middle. Their challenge (and opportunity) is to strengthen their position at the ends: as upstream tech specialists, or as downstream orchestrators.

A focus on the control and optimisation layer can lead to powerful position if the asset base grows faster than owners’ desire to build internal trading and optimisation teams. The control layer may be one of the most strategically attractive parts of the market, while also being one of the most exposed to consolidation and margin pressure.

A quieter but increasingly important layer sits beneath both the home-electrification story and the distributed-flexibility story: metering and control access.

metrify’s partnership with Macquarie is a good example. On the surface it is a smart-meter deal. In practice it is more than that. Smart meters are one of the enabling conditions for dynamic tariffs, automated load management, and distributed flexibility. That makes metering less of a side issue than it first appears. It is a bottleneck technology with capital beginning to form around it. If rollout accelerates, the economics of home-energy platforms and distributed optimization improve with it. If rollout remains slow, some of the more ambitious distributed-energy claims remain constrained.

Then there is the backbone itself.

Here the tone changes. The transactions around TenneT Germany, Amprion, and related grid funding feel like a system realising that the network itself has become a strategic asset class.

The TenneT Germany transaction brought in sovereign and pension-style capital. Apollo’s structure around Amprion shows private capital willing to finance expansion around regulated network assets. Germany’s own move toward a state-backed position in TenneT Germany makes the same point from the public side. The grid is no longer background plumbing. It is at the center of the investment story.