Mapping the Industry II: The German Flexibility Market

Making connections. Compare and Contrast V.

OpenAI released GPT-5.5 and I’m putting it through its paces across a spectrum of projects. This post is a GPT-5.5-assisted follow-up from our last post, where we thought about Value-Chain/Wardley Maps for the German energy industry. It builds on previous Stratnergy material, in particular the Compare & Contrast series.

Well, you tell me whether this is useful. It's certainly not easy to generate. The content is the result of multiple iterations adding up to significant overall run-time. Editing remains very important. Graphics are becoming better, but there’s a point at which I stop optimising, as you’ll see below. The language mirrors some of the language used in Wardley/ Value-Chain-Mapping, e.g. ‘games.’

The short thesis…

The German flexibility market is differentiating into several control-point ‘games.’ Optimisers fight for the dispatch decision. Virtualisers fight for the asset-access interface. Structurers fight for the risk book and benchmark. Asset owners fight for sovereignty, lifetime value and bankability. Utilities and BRPs fight for hedge, balancing and customer-control positions. DSOs and TSOs pull everything back toward the node, connection, tariff and system-security constraints.

The battery is physically the same asset in each story. Strategically, it is not the same component. To a trader it is optionality. To a virtualiser it is capacity. To a financier it is a portfolio. To a DSO it is a node. To a retailer it may become a tariff proposition. To an open-source strategist it is a bundle of interfaces, data standards and testable operating claims.

That is why the value-chain-mapping lens helps. It allows us to integrate the perspectives of platform, aggregator, optimiser, trader through a unifying set of questions: which user need is being served, which value-chain component is being controlled, and how is that component evolving?

Why revisit previous episodes?

The earlier Compare & Contrast posts did useful work. Part I separated Suena, Entrix, Enspired and ESFORIN as different optimisation and trading offers.

Part II added terralayr and FlexPower, which forced a sharper distinction between virtualisation and structuring.

The later flexibility updates added capital flows, global trading houses, integrated developers, Kyon / TotalEnergies, Terra One, newer or potential new entrants like Tesla and Habitat, and the possibility of new performance-transparency norms.

The platform-thinking series gave us theoretical scaffolding: pipelines, platforms, aggregators, inverted firms, modularity, open interfaces and the energy smiling curve.

This revisit changes the unit of analysis. It asks where each actor sits on the value chain, what control point it defends, and which parts of the stack should be industrialised by open standards or open-source reference implementations.

The Value Chain (Wardley) Reset

A Wardley map has two disciplines that are especially helpful in energy.

The first is value-chain discipline. Start with the user need. Work downward into the capabilities and components required to meet that need. Visibility falls as we move down the chain: investor confidence is more visible than telemetry protocols; revenue stack is more visible than a BMS API; tariff design is less visible to a trader than to a DSO, but it may still dominate the outcome.

The second is evolution discipline. Components move from genesis to custom-built to product/rental to commodity/utility. That movement changes management method. Novel things need exploration. Custom things need learning and adaptation. Productised things need vendor selection, contracting and performance comparison. Commodity things need cost control, resilience and operational excellence.

The strategic questions then become straightforward but uncomfortable.

Why are we treating a commodity component as if it were proprietary?

Why are we outsourcing a novel component before we understand the need?

Which component is moving rightward faster than our business model assumes?

Where are we confusing a product, a service, an aggregator and a platform?

Which components should be open standards, and which should remain proprietary alpha?

In flexibility, those questions cut through the marketing. An API is not automatically a platform. A dashboard is not a strategy. AI language is not proof of differentiation. A virtual battery is a useful abstraction, but it still depends on physical availability, telemetry, settlement, grid connection and trust.

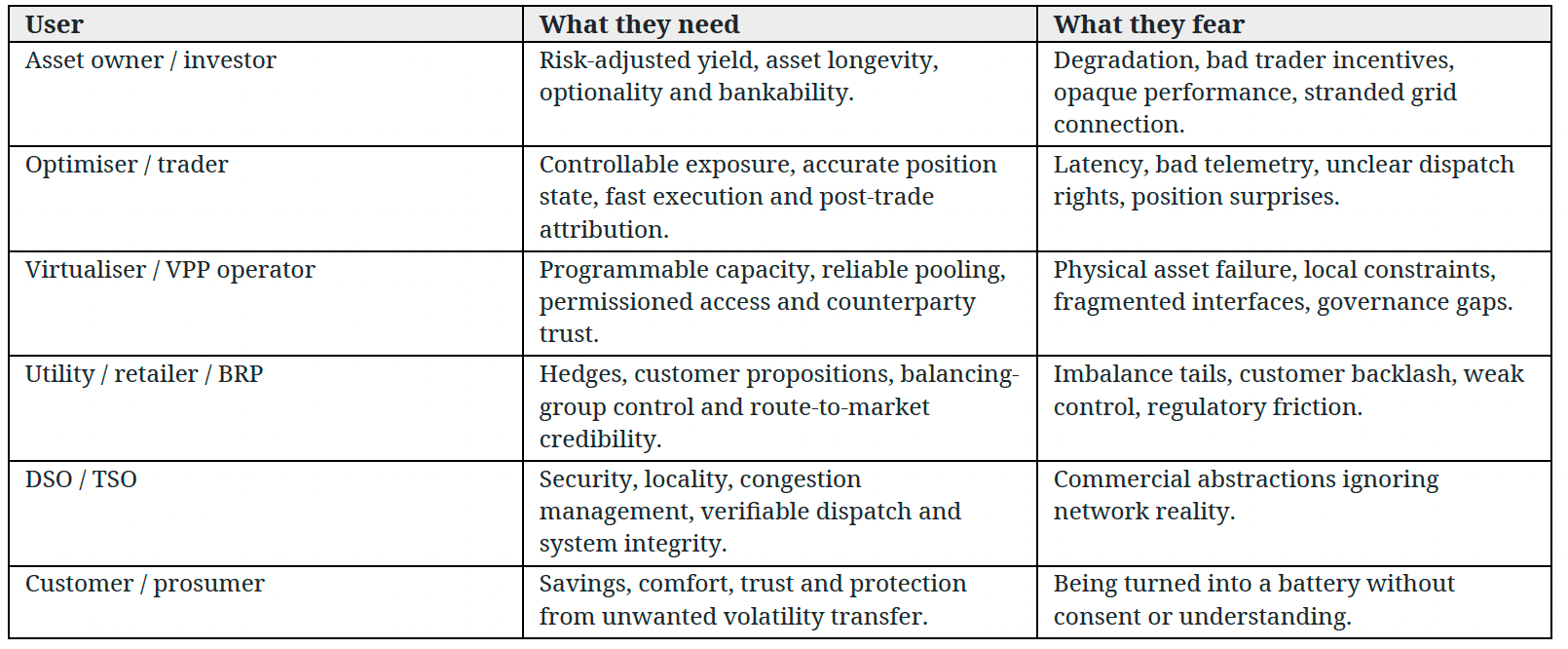

The anchor need: bankable flexibility under intermittent supply

The anchor need for this paper is not ‘battery software’. It is bankable flexibility under intermittent renewable supply. Bankable flexibility means flexibility that can be relied on, valued, financed, dispatched, settled, audited and repeated. That is a higher-order need than a single optimiser, VPP or battery project.

Different users express that need differently.