July 2026 European BESS transaction rankings

Trigger Warning: May involve projects mixed or smeared out in probability-weighted parts.

An AI supported review of BESS related transactions in Europe.

Let’s start with the most recent news: Alpiq is acquiring 90% of Harmony Energy.

Harmony reports to have developed, built and managed more than 700 MW across Europe and carries a development pipeline of more than 12 GW.

What is Alpiq getting by doubling down on Harmony (it previously acquired some of Harmony’s projects)?

It seems the idea is to acquire a machine for producing more projects: people, country organisations, grid-development capability, construction experience and an established route from site origination to valuable flexibility.

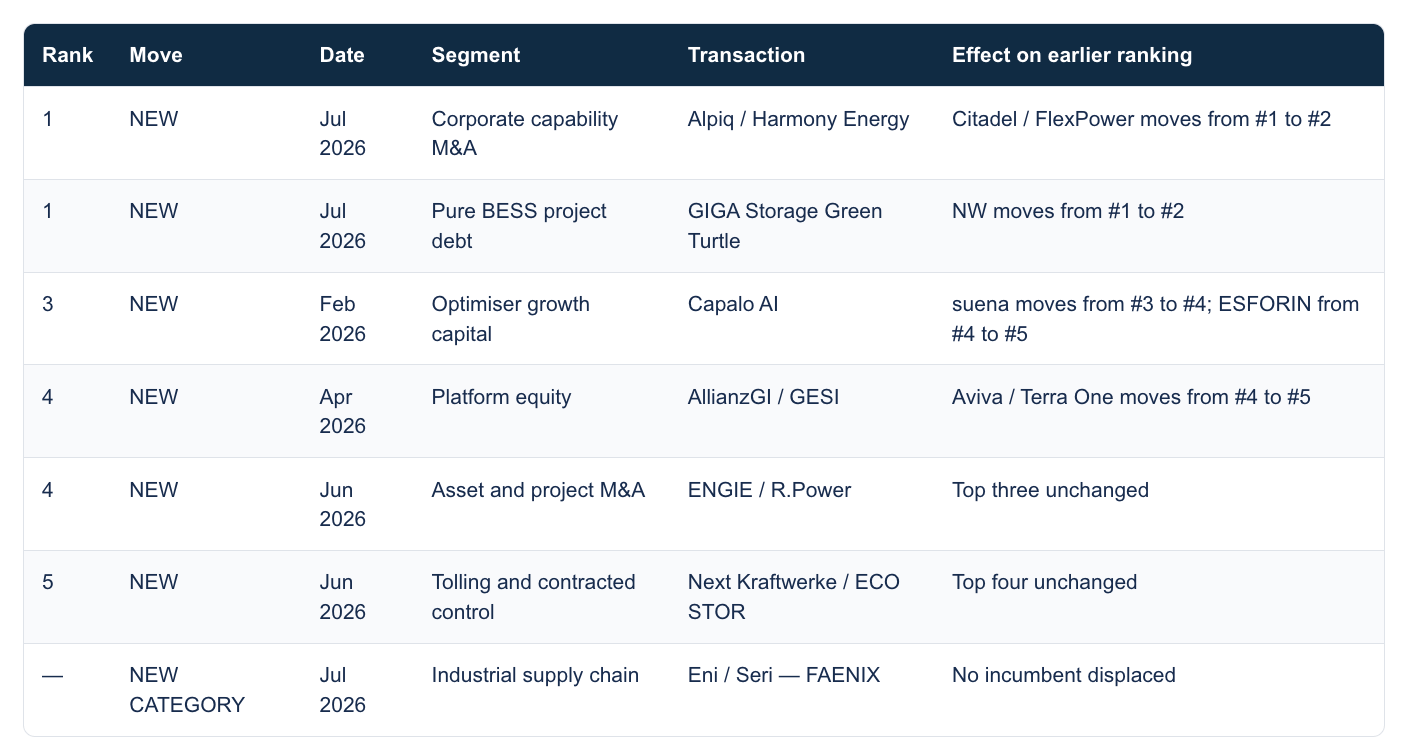

The disclosed consideration is unavailable, so we can’t rank on figures. It is, however, the strongest new entrant in our corporate capability M&A ranking.

Sources:

Ultimate harmony around this acquisition will likely turn on the quality of the pipeline. A pipeline is complex to value. You need to be careful with your probabilities… We’ll talk a bit more about the pipeline sensitivity below.

Ranking note

A €43 million optimiser round, a €450 million project-finance facility, a majority platform acquisition and a fifteen-year toll are not directly comparable: different claims on the battery stack. Not to worry, we can set things up the way we want to gain and maintain a picture of the market. Familiarity is the root of knowledge, right? And familiarity builds on structure.

The principal tables cover major publicly disclosed European BESS-related transactions announced or completed between 1 January 2024 and 15 July 2026. Movement is shown against the previous cut-off of 31 March 2026. Where a new entrant enters above an incumbent, the incumbent moves down.

A broader and more institutional transaction market

European BESS transactions have broadened from venture rounds and isolated project acquisitions into non-recourse debt, platform equity, strategic M&A, tolling, public-to-private transactions and supply-chain investment. We saw this last time.

Modo Energy’s transaction counts are one useful indication of that expansion, but the more important change is qualitative: recent deals disclose more about revenue allocation, dispatch rights, grid conditions and the division of risk between owners, lenders, traders and optimisers.

So, what’s new?

1. Optimiser growth capital

Gigawatts to survive (and thrive)?