Mercaptan in the Piazza: Oil & Gas Stress to BESS

Benchmarks and swaps, compare & contrast.

From gas in Italy’s merit order to Platts Dubai benchmark, comparing and contrasting indices and swaps for oil and BESS.

Walking the streets of Perugia you sometimes catch gas (mercaptan) odours. I noticed it most around the Arco dei Gigli. My mind inevitably drifted to the role of oil and gas in our economies.

Last time we looked at wholesale prices from Germany to Austria into Italy: an upward gradient into Italy NORD, where average prices are higher, which relates to combined-cycle gas being the price-setting technology a high proportion of the time.

Italy is among Europe’s most gas-dependent large economies, with gas accounting for almost 40% of total energy supply. 10% of consumption is usually imported from Qatar and Reuters reported that Italy is now in talks with the United States, Azerbaijan, and Algeria about replacement volumes after damage to Qatari infrastructure.

As I was reflecting on all of this I happened upon The Oil Bandit’s latest post, which describes the layered benchmark system around which Middle East crude is valued: the Platts Dubai process, linked swaps, and more liquid instruments such as Brent and the Brent-Dubai EFS. What can the BESS market learn from this system?

We have looked at relationships like this before, thinking about volatility across different markets.

This time our focus is on benchmark and market design, centred around the simplest of questions: what are we pricing? Headline price moves inherently involve a story about benchmark design. How are oil price benchmarks designed? What can the BESS asset class learn from the more mature oil & gas markets?

In the Corriere della Sera, Federico Fubini pointed out that the oil market has “split in two” and then gives the comparison directly: Brent around $114, Dubai around $136, and Oman around $153. What exactly does it mean to say that “oil is up”? Which oil? Priced how? Through what instruments? Against what delivery assumptions?

L’aumento vertiginoso degli indici di greggio Dubai e Oman si spiega con il fatto che essi sono divenuti molto più scarsi con la chiusura di Hormuz. Dunque, molto più cari. Ma presto le raffinerie asiatiche, dopo aver consumato un po’ delle loro scorte, potrebbero entrare in concorrenza con le raffinerie europee e americane per il greggio occidentale venduto ai prezzi del Brent e Wti. E una maggiore domanda non può che far convergere i prezzi del petrolio consumato in Europa, al rialzo, verso quelli del petrolio consumato in Asia. In altri termini, potremmo dover assistere ad un altro strappo al rialzo del Brent, che già da questa mattina si inizia a vedere.

The meteoric rise in the Dubai and Oman crude indices is explained by the fact that they have become much scarcer with the closure of Hormuz. Therefore, much more expensive. But Asian refineries, having used some of their reserves, could soon enter into competition with European and American refineries for Western crude sold at Brent and WTI prices. And increased demand can only cause the prices of oil consumed in Europe to converge, upward, towards those of oil consumed in Asia. In other words, we could be witnessing another upward surge in Brent crude, which is already beginning to be seen this morning.

The Oil not Dead note focuses in further on the question of what an oil ‘price’ means. An important part of this machinery in focus through the current situation is Platts Dubai, which S&P describes as the physical price of Dubai crude loading through the relevant month, reflecting the repeatable, transactable price of crude loading two, three and four months ahead of the assessment date, using bids, offers and trades in the Market on Close process.

This benchmark enables a “swap” layer: Dubai-linked swaps are contracts that settle against the benchmark. These swaps are standardised enough to anchor a regional hedge market, and are best thought of as a family of benchmark-linked instruments.

The Dubai benchmark provides a reference point for more regional or specialised grades and markets. Currently, for example, immediate Oman and Murban barrels are worth more than the paper Dubai benchmark for the same month.

Spot premiums for Oman and Murban futures to Dubai swaps also surged to more than three-year highs of $5.51 and $6.52 per barrel, respectively. Source Link

So we have regional benchmarks, which support families of financial hedges/ instruments and provide reference points for more specific transactions. Regional market dislocation can be measured quite precisely by comparing sub-regional contract value to the regional benchmark.

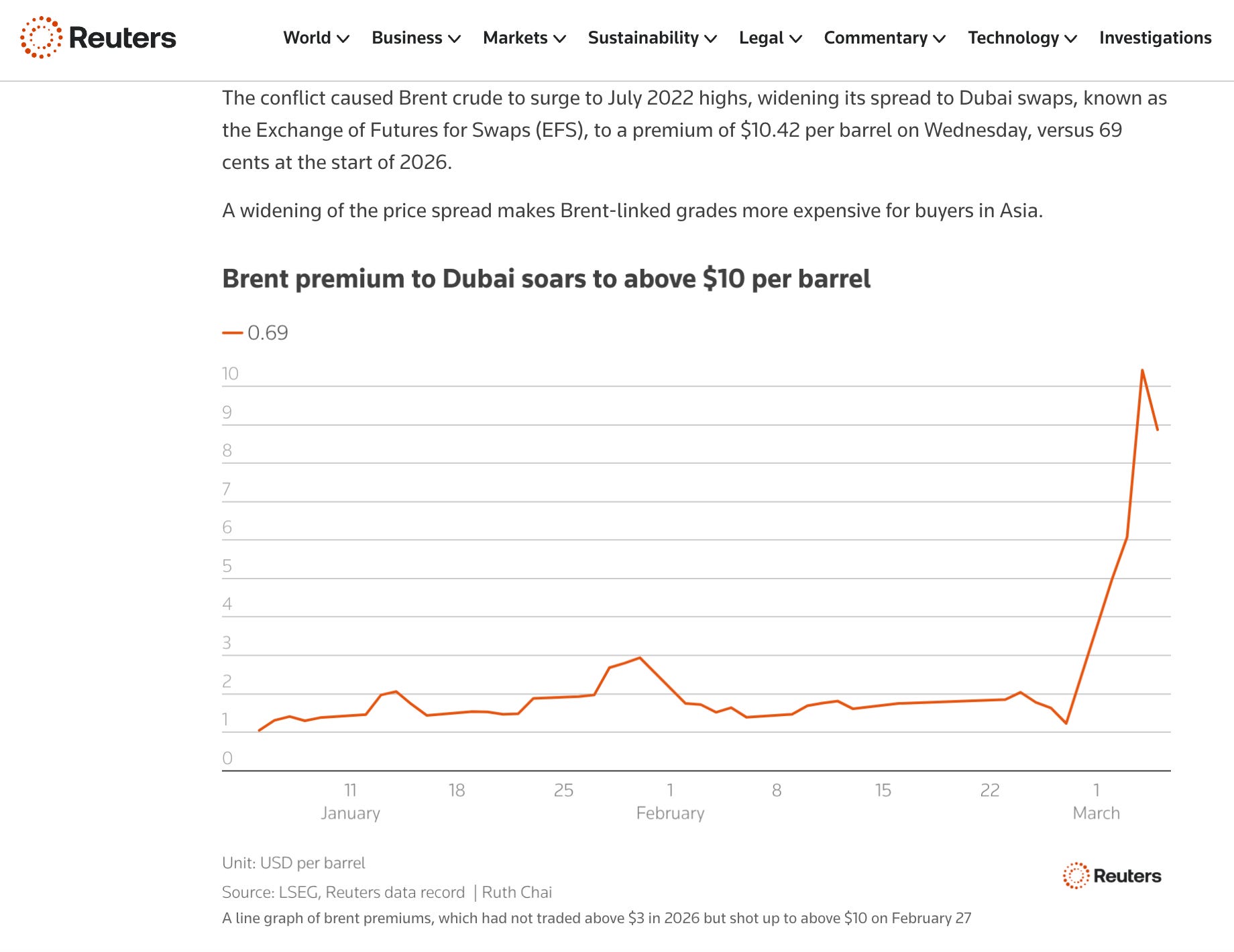

Zooming out, the larger-scale dislocation can be measured by comparing regional and global benchmarks. Brent futures are the deep, liquid global crude contract, whereas Dubai-linked pricing is the main sour-crude reference used across Asia and the Middle East.

The Brent-Dubai EFS (Exchange of Futures for Swaps) is the spread that links the two. It is the spread between Brent futures and the Dubai cash market, i.e. what it takes to exchange a Brent futures position for a Dubai swap position.

Brent and WTI are the world’s major benchmarks. They have attracted the deep financial markets that solidify their usefulness and status. They are so overwhelming that they overshadow all other initiatives trying to gain market share. Creating benchmarks takes time. In the Middle East, Dubai and Oman are benchmarks for pricing medium, sour oil. But they essentially trade at a differential versus Brent. Trade in Dubai and Oman fine-tunes the spread versus Brent as expressions of the quality differential between sweet and sour grades and the geographic differential between the Atlantic Basin and Asia.

What looks, from a distance, like “the oil price” is therefore a layered system: benchmark assessment, derivative overlays, and more liquid futures around them. Under normal conditions, that structure mostly disappears behind a single number. Under stress, it comes back into view: good benchmark machinery makes the stress visible. Consider two examples.

TotalEnergies was reported to have bought a significant number of Oman and Murban cargoes just as the pool of crude eligible for the Dubai benchmark process had been cut back sharply. At the same time, Oman and Murban prices jumped relative to Dubai swaps. The physically available crude inside the system had become scarcer and more valuable, and so aggressive buying in the benchmark window suddenly mattered much more than usual.

A Japanese refiner reportedly bought 2 million barrels of U.S. WTI for June arrival as an alternative to tighter Middle Eastern supply. On paper, the crude itself looked competitive against Dubai-linked pricing. But once freight costs were added, the delivered cargo ended up costing roughly $10 per barrel more than Dubai. The lesson? In times of stress, you need to look beyond the benchmark! When regional barrels become hard to get, buyers can try to replace them with oil from farther away, but the replacement is not judged only by its headline price.

Now, do aspects of this seem familiar in the context of BESS? The connection is not as far-fetched as you might think.