June, Germany: catch-up

With a focus on reserves

Reserve capacity is like an option premium. Activation is the option being used. The first ten June delivery days gave both sides of that trade: evening scarcity, an intraday price break, and midday surplus that mostly stayed in aFRR- but reached mFRR- on Sunday.

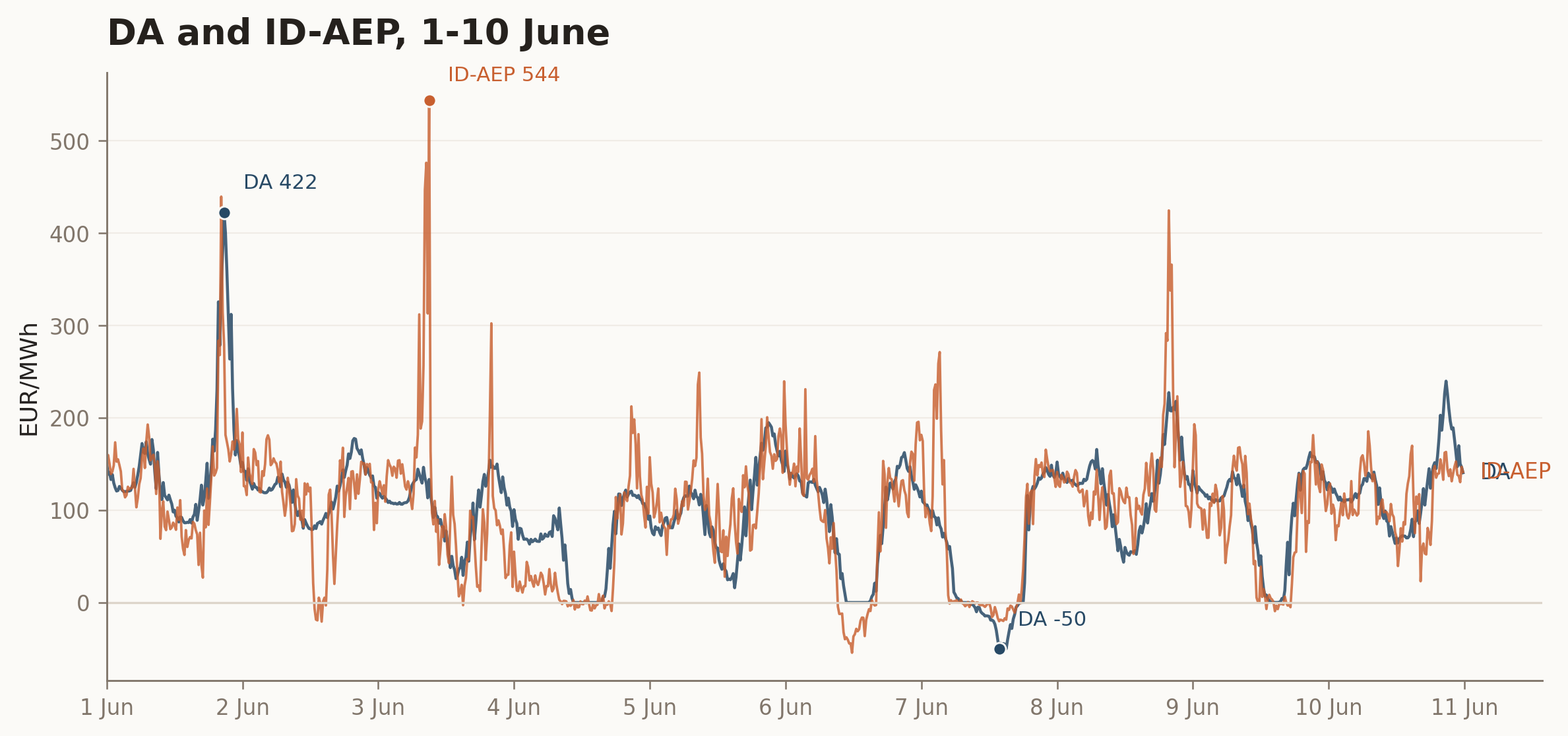

1 June squeezed the evening. Day-ahead reached 422.28 EUR/MWh at 20:45. Reserve prices moved with it: aFRR+ 20-24 cleared at 106.41 EUR/MW/h, mFRR+ at 74.10 EUR/MW/h, and FCR 20-24 at 112.62 EUR/MW/4h.

3 June featured an intraday break. Day-ahead was firm. ID-AEP, the German intraday auction ex-post index, broke loose: 543.92 EUR/MWh at 09:00, against 133.27 EUR/MWh in day-ahead.

Then came two surplus days. On 7 June, day-ahead went negative for 41 quarter-hours. The low was -50.25 EUR/MWh. Renewable output pushed the system deep into surplus; Sunday ranked 29/159 year-to-date on renewable share of load.

Options in reserve

Three cases matter: 1 June evening, 7 June midday, 9 June midday.