ID-AEP, BMRS MIP, and Two Ideas of What Markets Are For

UK vs Germany, III.

What is the value of flexibility in a crisis, and why does that value look different across markets? To answer that seriously, we need public price signals that let us compare short-term market conditions across systems. Germany offers an unusually useful open proxy in ID-AEP. Great Britain has no exact equivalent, but its BMRS Market Index Price serves a comparable role. Placing the two side by side reveals different approaches to flexibility and imbalance.

One system seems to begin from the fear that flexibility will produce bad feedback unless tightly bounded. The other seems to begin from the hope that flexibility can be taught to behave well if the incentives are right.

Please remember that optimism and pessimism are definitions of the world, and that our own reactions on the world, small as they are in bulk, are integral parts of the whole thing, and necessarily help to determine the definition. They may even be the decisive elements in determining the definition. A large mass can have its unstable equilibrium overturned by the addition of a feather’s weight. A long phrase may have its sense reversed by the addition of the three letters n, o, t. William James

I have previously argued that German energy-market design reflects a broader stability culture: balancing groups are expected to keep quarter-hour deviations small, balancing energy is meant to correct what could not reasonably have been predicted, and institutions worry that too much real-time visibility might encourage overreaction.

Too afraid of strange loops?

“Deep understanding of causality sometimes requires the understanding of very large patterns and their abstract relationships and interactions, not just the understanding of microscopic objects interacting in microscopic time intervals.”

In this narrow but important sense, Germany’s balancing world is a planned economy. Every quarter-hour is supposed to add up. Purposeful imbalance is streng verboten. It is not seen as a potentially legitimate contribution to system correction, but as a breach of balancing discipline.

“The aim… is to stop the wrong kind of incentives. We want to prevent imbalances in the German electricity system such as the severe ones that occurred in June 2019,” said Jochen Homann, Bundesnetzagentur President. “ This decision completes the measures designed to improve the upholding of balancing group commitments.

Source Link.

In contrast GB’s imbalance is more openly cashed out by the system rather than folded into a broader ethic of plan-fulfilment.

Previous UK/Germany essays have developed this point more broadly: in Britain, data tends to function more openly as a coordination signal; in Germany, data more often sits inside a regulatory toolset whose purpose is to make institutional reasoning nachvollziehbar.

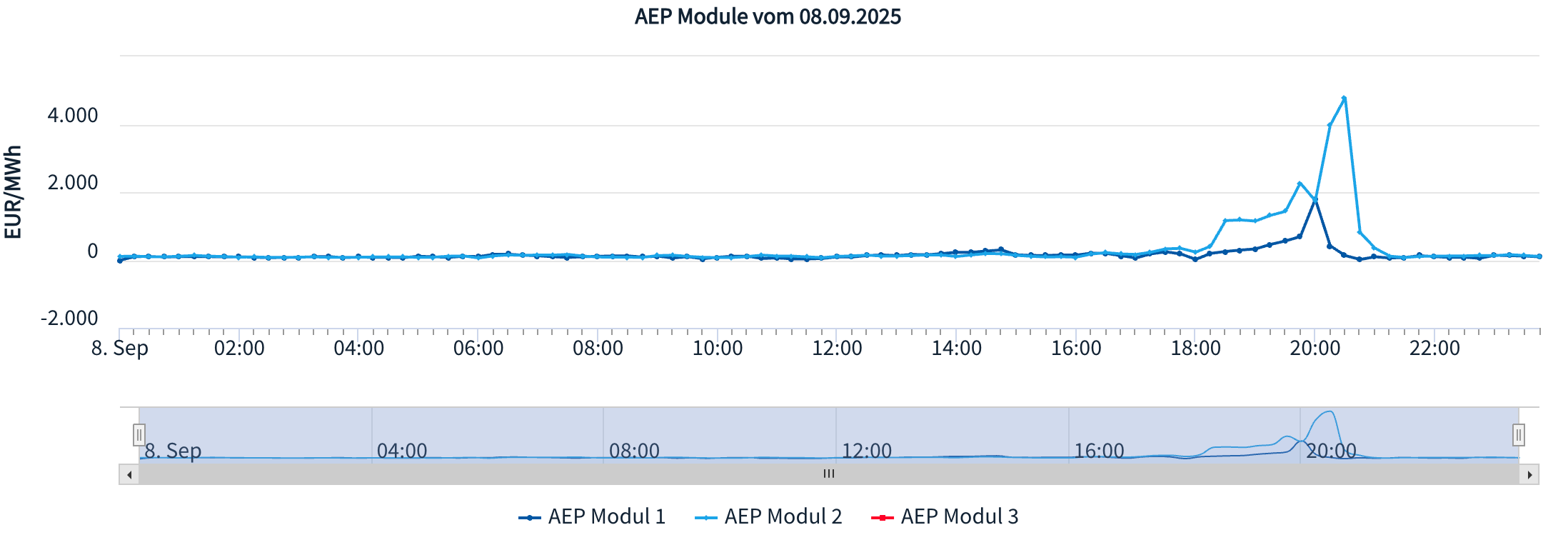

So let’s consider Germany’s ID-AEP, which I think is revealing of the German arrangement towards imbalance in its system.

Netztransparenz defines the ID-AEP as an intraday price index built from the continuous intraday market in Germany, using the last relevant trades closest to delivery, with a liquidity threshold: the index is formed from a volume-weighted average once at least 500 MW of trading volume is reached.

ID-AEP contributes to the German imbalance price, reBAP used to settle balancing-group imbalances: flexibility of the short-term market is folded into a top-down settlement architecture for remaining imbalances between planned and actual.

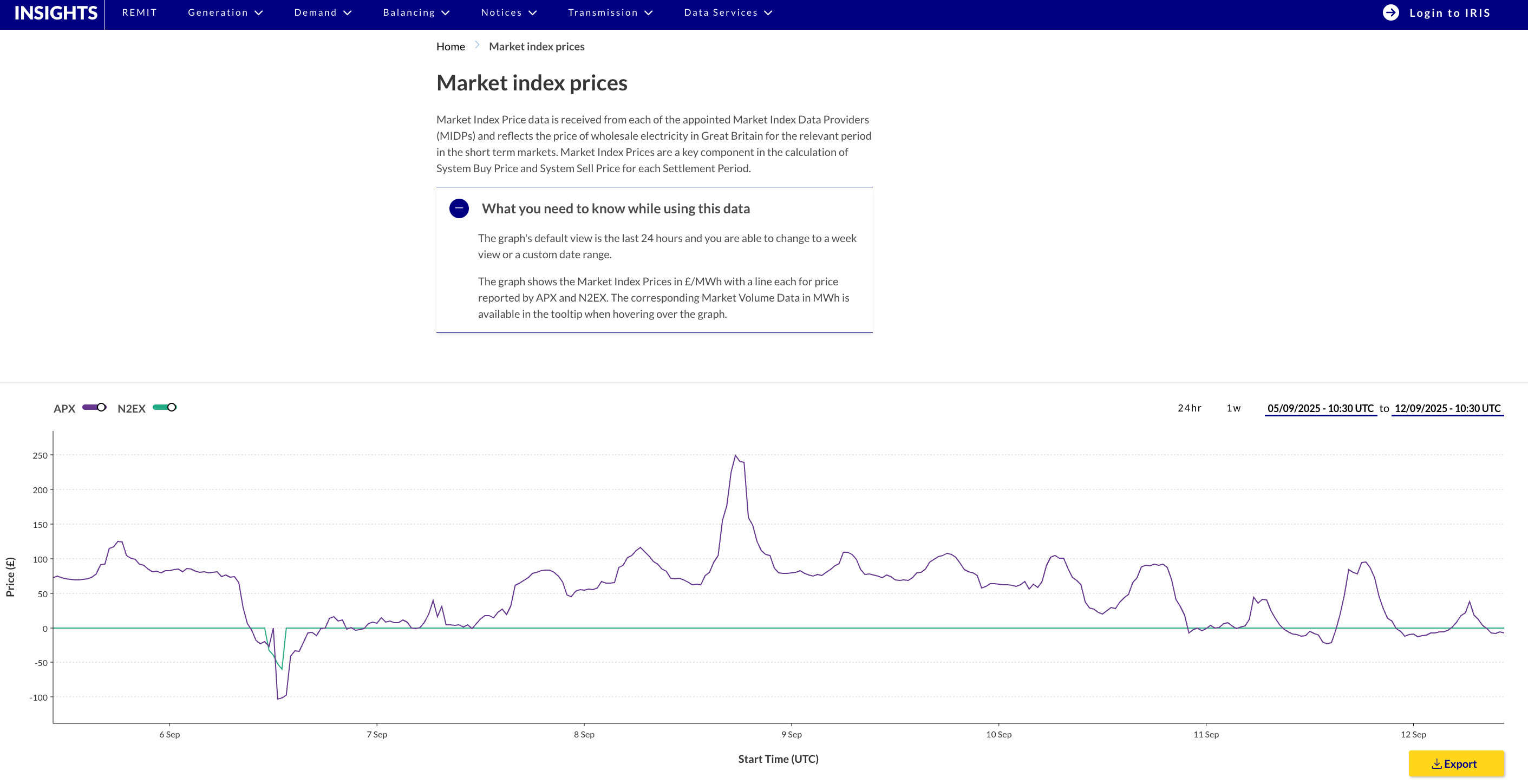

Britain’s short-term imbalance world has a different feel. Market Index Data (MID) is used to calculate the Market Index Price for each Settlement Period and reflects the price of wholesale electricity in the short-term market.

The imbalance price is used directly to settle the difference between a party’s contracted and metered position in each Settlement Period. The system is built around cash-out of that difference. Parties can seek to mitigate their imbalance position closer to real time, and that more real-time information can help them reduce their exposure to the imbalance price.

In other words, Britain still wants parties to contract properly and avoid imbalance, but the mechanism is different: the system is more willing to let imbalance be priced and managed ex post, rather than treating the quarter-hour balance as a quasi-constitutional duty in the same way Germany does.