Germany's Asynchronous Transition: Data, Decoupling, and the Gridlock of 2026

Data Report — February 2026 | Sources: MaStR, TSO Data

This is an article co-generated with an agent running with but not confined to OpenClaw. Please let me know if you find any mistakes. I found it fascinating to run through the German energy situation at this level, and I hope you find this useful or interesting. Also available at https://stratnergy.online/research/german-energy-transition for signed up subscribers.

Summary: Germany has reached an inflection point — 232 GW of renewable capacity but a grid that can’t transport it. This report analyzes the geographic, temporal, and financial dimensions of this “asynchronous transition,” from state-level storage gaps to BESS pipeline trends to redispatch costs. The bottom line: more storage is needed, and fast.

Key Takeaways:

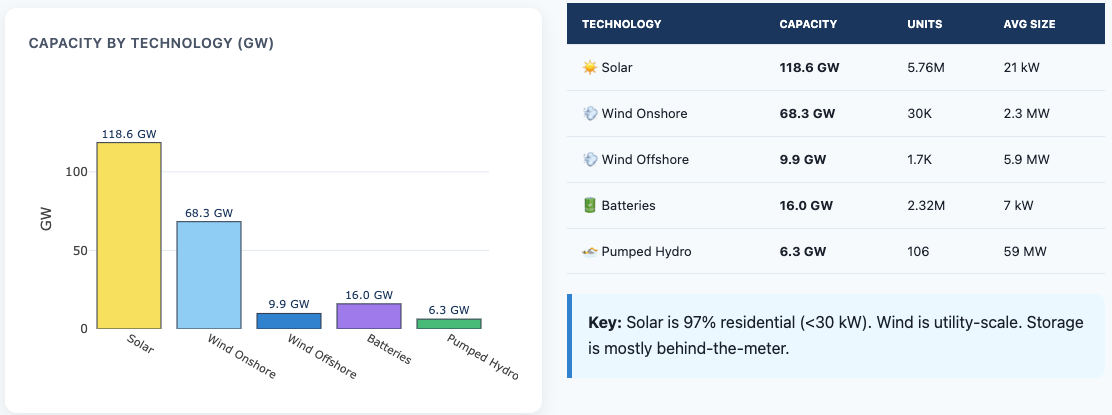

232 GW renewables — but grid bottlenecks cause 20.5 TWh curtailment (64% renewables)

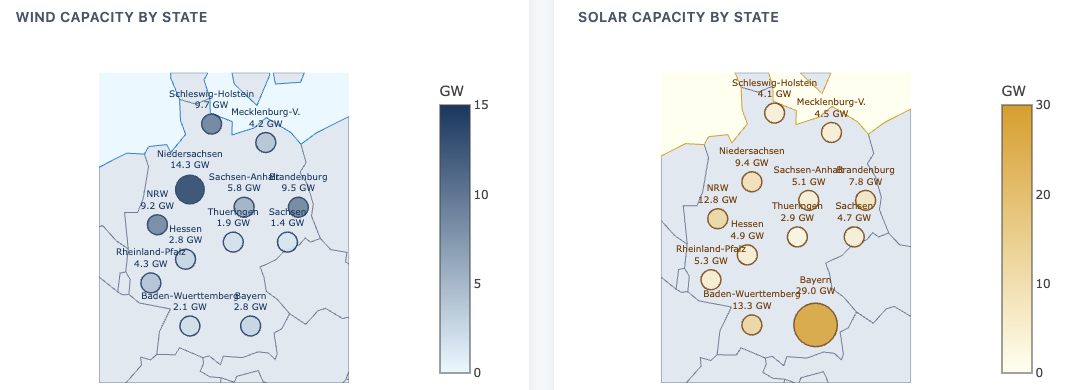

Geographic mismatch — wind clusters north (NI 14 GW), solar dominates south (BY 29 GW), transmission limited to ~10 GW

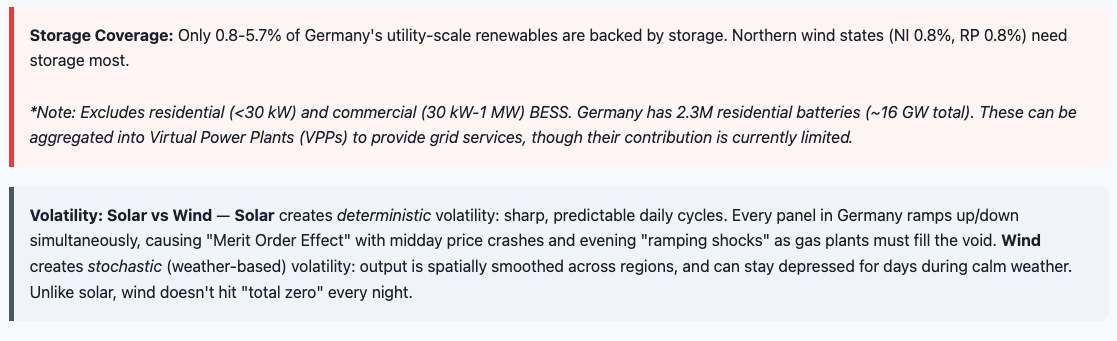

Storage gap — only 0.8-5.7% of renewables backed by storage; grid-scale BESS (>10 MW) is just 1.6 GW

€2.8B cost — redispatch compensation passed to consumers; ~5M tonnes CO₂ “transition penalty” (upper bound)

Pipeline looks promising — 5.7 GW BESS planned, concentrated in northern states where storage is needed most

1. Generation Mix

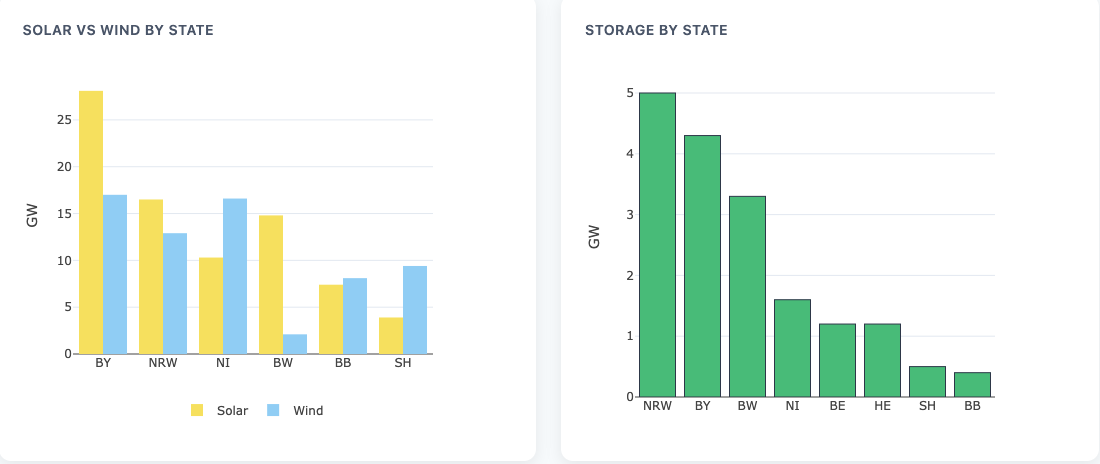

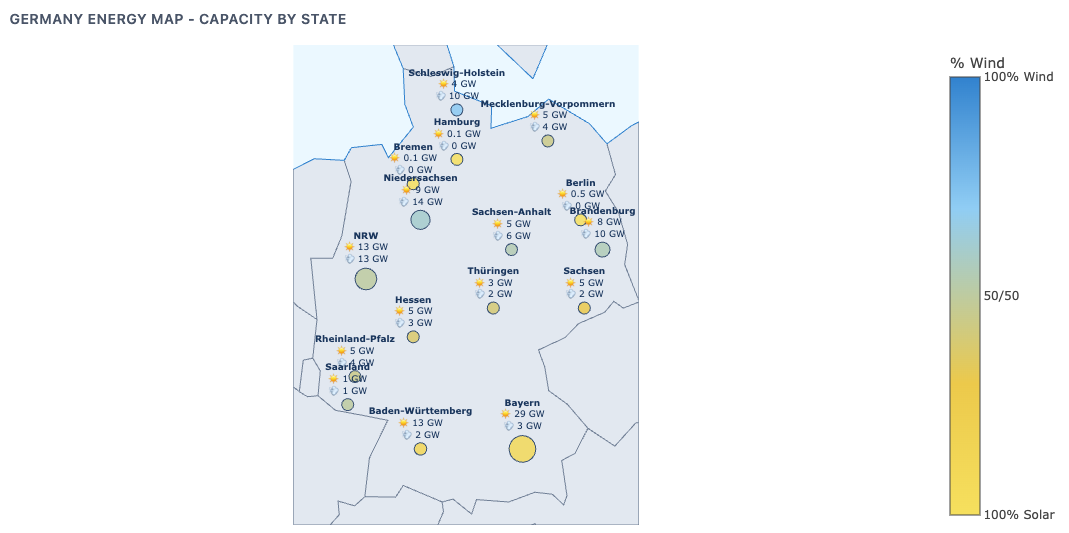

2. Geographic Distribution

German State Abbreviations: NI=Niedersachsen, MV=Mecklenburg-Vorpommern, ST=Sachsen-Anhalt, BB=Brandenburg, SN=Sachsen, TH=Thüringen, RP=Rheinland-Pfalz, HE=Hessen, SH=Schleswig-Holstein, NW=Nordrhein-Westfalen, BW=Baden-Württemberg, BY=Bayern, HH=Hamburg, HB=Bremen, BE=Berlin.

A look at relative share of wind and solar across Germany.

3. Renewable Energy & Storage Coverage

4. Grid Stress: The North-South Problem

The fundamental problem: Germany’s grid wasn’t built for this. The issue is TWO-FOLD: